3. Ontario Case Study - 3.1. Provincial Design & Local Response

One of the challenges tucked into ‘rebuilding better’ is reconciling the shared interest in enhancing municipal resiliency with one of the cumulative effects of understanding municipalities as ‘creatures of statute:’

expectations of financial dependence are baked-in.

This article traces the roots of the expectation to the design of municipal institutions; that is, formal rules set out in provincial legislation about municipalities’ purpose, powers and exercise of them. This situates patterns of local decision making and financial behaviour in municipalities’ historical and legal context. It finds that local actors respond to municipalities’ institutional weakness in ways that reinforce it.

There are two reasons for this approach:

Many people recognize that municipalities operate within a provincial framework, but underestimate the softer, cumulative impact of written rules on culture and expectations. The space between the subsection of an Act indicating what municipalities “may” or “shall” do, and a headline about what a Council did weighs heavily on the options that Council saw and selected, however credit is rarely given its due, which negates governance design as a practical constraint on local decision making.

Sidestepping the soft, invisible influences of institutional design on local decisions relieves designers of accountability for how the systems they create actually work. By not tracking how design constrains, or frames, local choices, neither can municipal actors be held accountable for the latitude they enjoy within constraints.

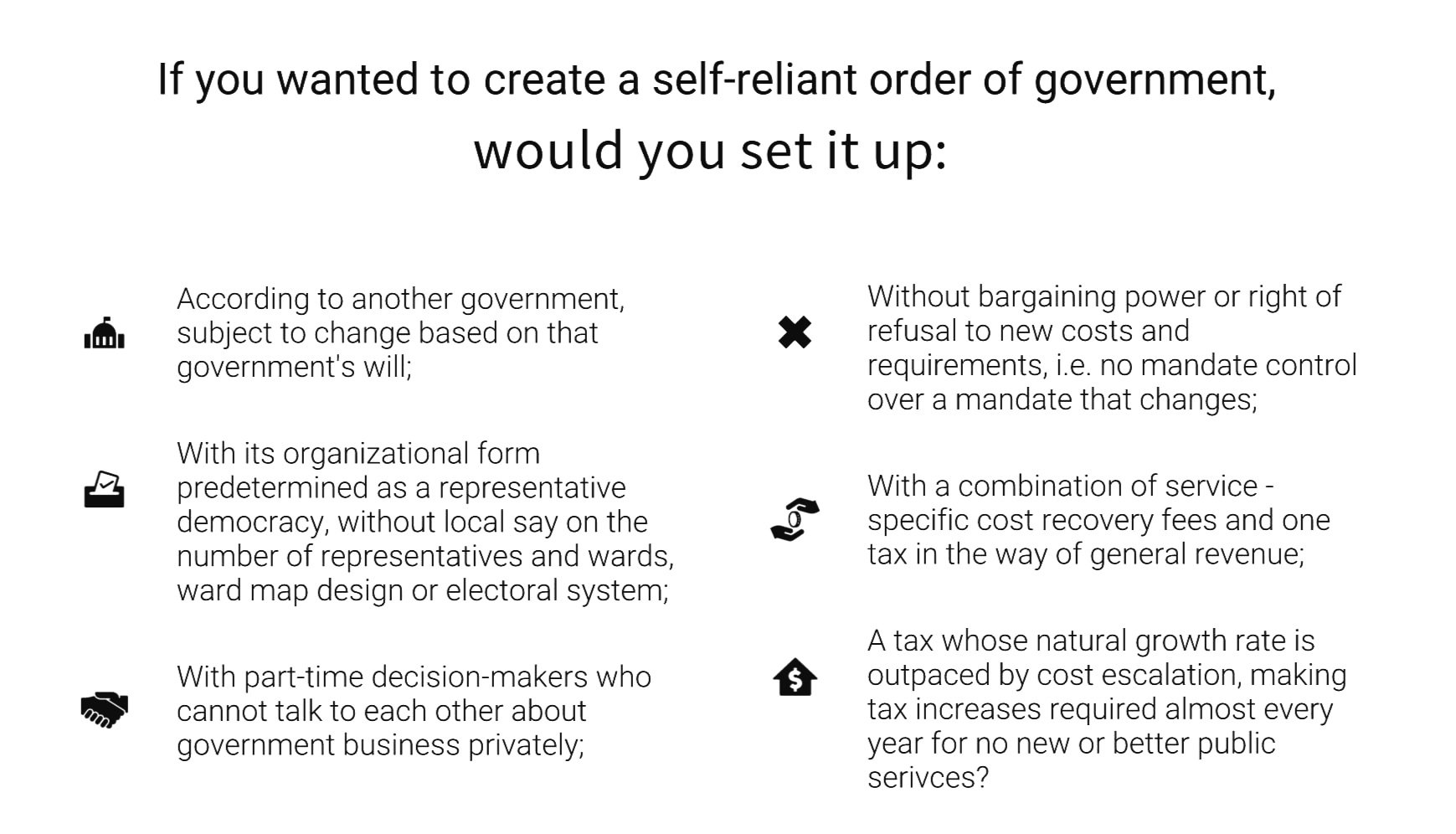

Governance Structure

Rules are the common legal reference point for what constitutes acceptable behaviour in a group. They shape what people think municipalities are supposed to do, which influences who they vote in to do them, how those people think they are supposed to govern, what they think they are supposed to do, and how staff understand their role.

Evidently not, since the decision-making environment created by the design pre-conditions municipalities to sub-optimal outcomes. Therefore, the premise of the exercise is flawed: If you wanted to create the kind of institution the Ontario Government indicates it wanted to create in municipalities, it would not have outfitted it with design features that predispose individual municipalities to controversy, underinvestment and regulatory co-optation. Intentions will likely remain private, but mapping the local impact of a system with major provincial inputs can be suggestive; if the system weren’t functioning as intended, it would be changed accordingly.

2. Local Response

How does ‘dependent by design’ effect municipalities’ financial stewards - professional staff and members of Council?

Self-concept and Expectations - Created, terminated and changed through different kinds of written rules and requirements, municipal actors are geared to understand municipalities’ purpose and scope on external terms, i.e. parking and bike lanes are hot issues, and how many municipalities considered sending police troops towards Ukraine’s defence? (For contrast, the City of Evanston, Illinois, was the first arm of US government to supply reparations to African Americans (Moscufo, 2021).)

Information Asymmetry - After running a campaign and winning a seat in a democratic election, the same way federal and provincial representatives do, members of Council enter government and learn that they can be overruled by an administrative tribunal. The perceived-actual scope gap creates a learning curve for members of Council that, anecdotally, takes half a term to get up. If there’s one thing they know, it’s that the public does not understand the power of the province in, to and over municipalities, and they may use the asymmetry for political advantage.

Political Use of Asymmetry - Where a Council wants to say no, or is not ready to make a decision, members can point to an outside authority’s rules or project as the reason for why, Our hands are tied, as it were, whether valid, complete or otherwise. Here, actual institutional weakness is compounded by the political benefits of weakness to the detriment of political accountability for financial results and revenue decisions.

Unassessable - Without existential sustainability, financial sustainability for municipalities is technically a moot point. Practically, it makes assessments of financial performance limited to discretionary operations and related decisions, and in the normal course of work, no distinction is made between mandatory requirements and service standards, and the actual day-to-day service levels provided. Neither is financial information presented according to degree of control, so the information that people would need to evaluate a Council’s fiscal record is not compiled internally or supplied externally. Since staff are the only group who could supply it, that they don’t supply it - information no one is asking for, and Council may discourage staff from supplying – sets up a situation where they inadvertently contribute to the difficulty the public faces in evaluating the quality of a Council’s decisions.

Transformational and public trust-building work de-centred - Outfitting municipalities with a dual provincial and popular mandate to serve everybody 24/7/365, and change on demand, has kept staff busy, without much time for unstructured, non-incremental thinking. Jeff Bezos credits this kind of “wandering, … not obvious how they’re going to work out” thinking with getting him into space, so it’s also possible that a side-effect of over-run administrators is rote operations. Financial reporting requirements that absorb significant staff time in small municipalities gear fiscal accountability more to the provincial government than the local community.

Staff Relay Limitations, Source of Tension, Potential Distrust - In Ontario, the same provincial law that sets municipal jurisdiction and Council authorities tells municipal treasurers that their job is to provide information Council “requests or requires,” thus, bridge the gap between its perceived and actual scope. One element of any government’s impact is effective use of the bureaucracy and the combination of weak municipal literacy among the general public and staff designation as intermediaries predisposes the Council-staff relationship to friction.

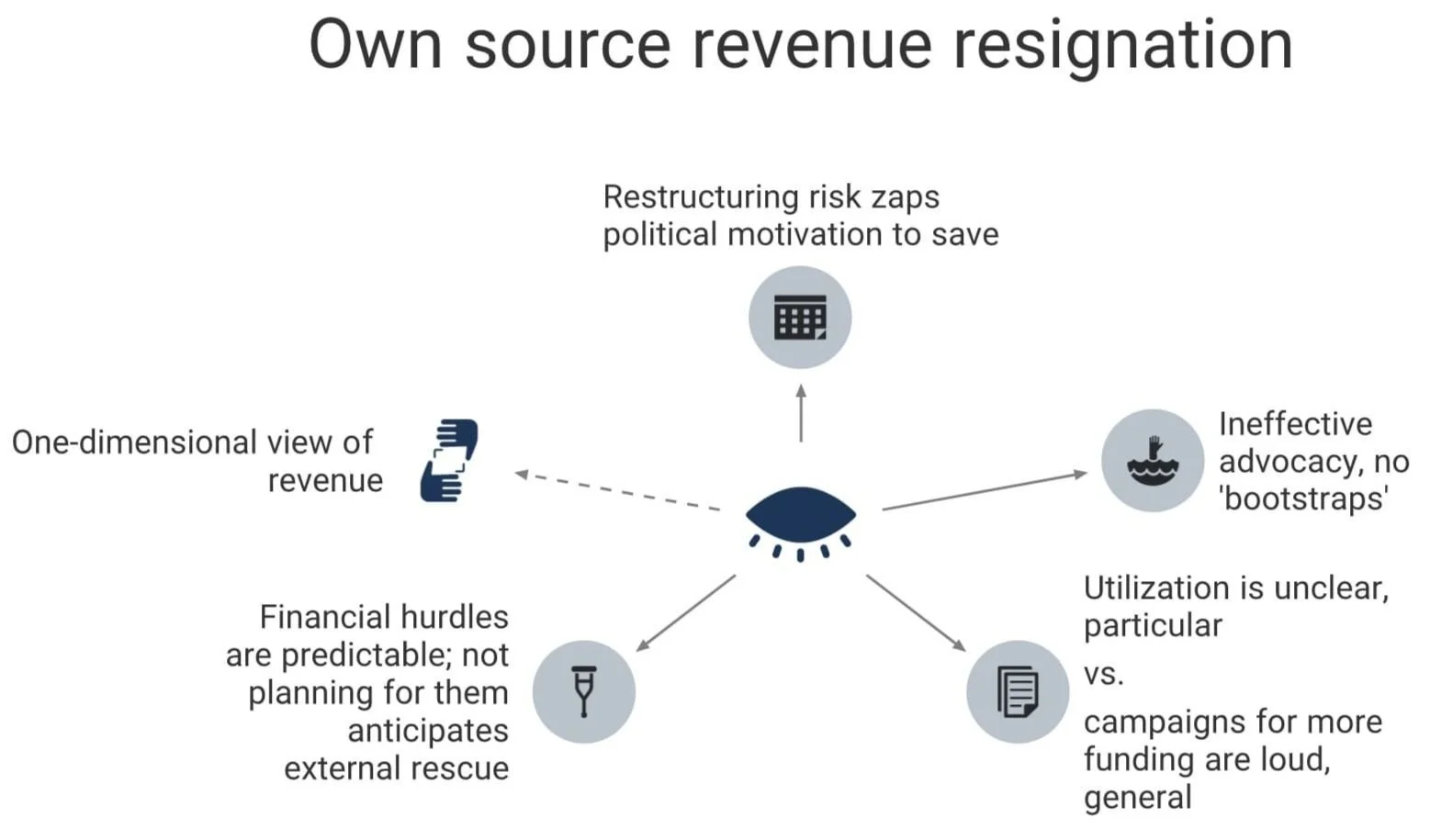

Own Source Revenue Resignation - Pre-pandemic, the lack of depth, breadth and manoeuvrability were well-known characteristics of the municipal revenue system that municipal advocacy did little to change. From their persistence, we know that, according to the system’s architects, it was okay if things got ugly for municipalities; it’s not the province’s role to prevent financial crises within delegated authorities, or not their priority, in any case. Raising a red flag and it not being acknowledged as a problem worth solving by those with power to solve it has cascading effects on organizational behaviour and fiscal agency:

Taxing today for contingencies tomorrow is especially challenging for governments that may not exist in the short, mid- or long term, so it follows that some of their political stewards act like it and do not plan or save enough. A ‘live for the day’ kind of short-term thinking can take hold on Council, and it appears that some representatives believe that, if it’s solvable, municipalities’ financial fragility is a problem for the province to solve, or maybe big cities.

While ‘it’s outside my scope,’ or ‘its outside the expectations of my office,’ are understandable takeways from the formal, legal, operating context, it’s also true that big financial challenges are predictable for municipalities. The question isn’t ‘if’ they will happen, but ‘when.’ By not deciding how the municipality will handle new pressures and planning for them using the law-making and revenue-generating handles available, these members also put a solution outside their scope.

It normalizes dysfunction and begets complacency in the management of existing own sources. Yields are not determined by revenue-raising powers, so the vagueness of how one municipality uses its existing capacity to generate is easily overshadowed by rejected requests for broader authority and new tools. Advocacy messaging narrates and research creates a paper trail making the case for Councils: “we don’t have the tools for the job,” still leaving observers to fill in the gap - if there were more revenue to be yielded from existing powers, municipalities wouldn’t need to agitate for more. As such, it curtails expectations that municipalities will be independently responsible for fiscal self-help in a crisis.

Lack of cohesion between functions - In whatever kind of government, elected officials appear to prefer that staff handle the issue of how to pay for their plans. For municipalities, this means that the values questions about who should pay go unacknowledged by one of the only bodies with the power to tax. The appropriate mix of revenue sources is not the subject of direct Council discussion and decision, so there is neither a revenue strategy consistent with other government functions in most municipalities, nor political accountability for the risks inherent in pursuing one course of action over another. As such, incidence of payment may well undercut the reason for spending.

These are some of the ways local actors interpret and respond to their legal environment that, while entirely understandable and partially conditioned, are not predetermined and contribute to sub-optimal financial results.